Despite competition between mega builders of aircraft and inspite

of active sales efforts a waning of the order book is predicted for 2017.

Boeing and Airbus both have a trend breaking scenario thrown in the way. The

trend is for quiet sales placed during 2017. The best way of analyzing the

2017 projection is to go model by model pass fail grading or assigning a

letter grade for each class and a certain indicator is giving a P/F designation

with a dashed letter grade.

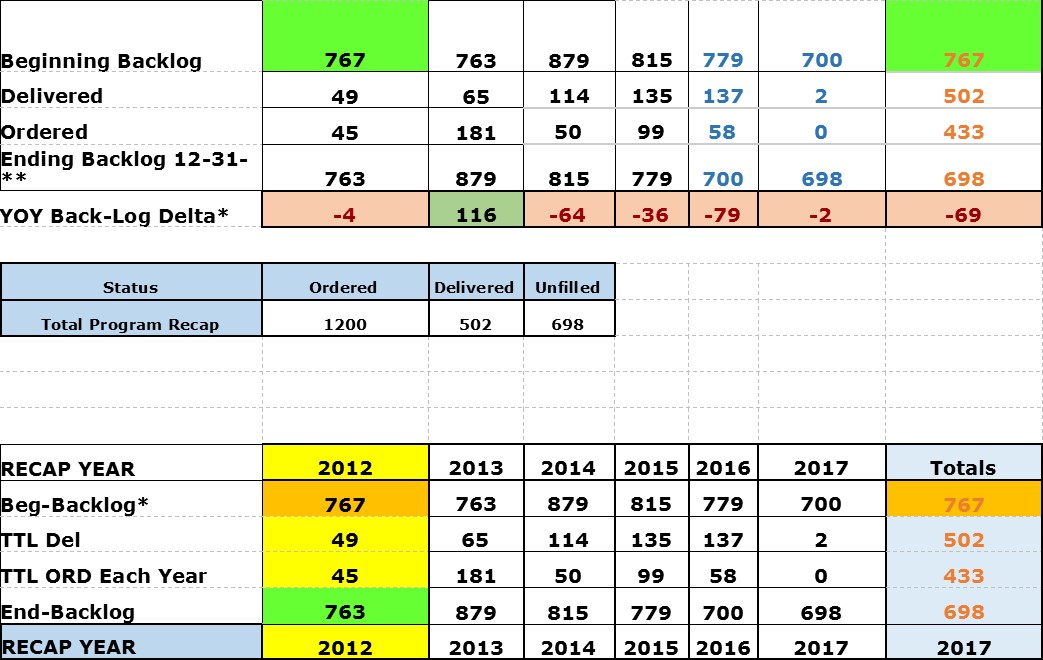

737 Family P-C+

767 Freight F-D

747 all F-F

777 ER or X P-C-

787 Family P-B-

GPA= 1.6 (probation)

Boeing is facing mediocrity of a classic nature. Those class of

aircraft on a life line will implode and those aircraft that are the

"stars" will fight to stay awake. There are a few surprises coming in

2017 and a few disappointments coupled with having a wake for the 747.

The 737 family will continue to pop corks with cheap wine in break

rooms around the Boeing world. The 767 freight division will go zip for half the year and then

the KC-46 comes out to play receiving its well earned D and a Failed order

book.

The 747 is dead on arrival as the backlog evaporates during 2017.

Even a lucrative AF-1 contract with the US government is a fitting farewell as

Trumps looks at the last big American show goeing by the way of the

Barnum and Bailey Circus.

777 is the poster child for the buying appetite of great airplanes

during 2017. It will have a "meah year", as the big players have

weighed during the last three years. The 777X could be a second year no-show

while the 777-ER should pick up all the leaner's from last year.

The 787 is an order book juggernaut. It took in about 68 orders in

2016 and it has possibilities to exceed that number for 2017. A wishfully

optimistic prediction is a 100 787's or a more cautious sane view is for 40 in

the upcoming year grading out at B-.

The GPA is probationary and it represents the buying sources to be

maximized from the last five years. This hold true for Airbus since it is

difficult to find who would place an order that hasn't already placed an order.

Only successful customers from the last two years have incentive to buy its

favorite aircraft going forward.

The year 2017 may become a C- year and a Pass for Boeing.

Here are Wild Analytical Guesses (WAG) or orders for the line-up.

2017 WAG:

737 Family 550

767 Freight 6

747 all 0

777 ER or X 20

787 Family 40

Total 616