The 747 was an over built giant

that determined how many seats is needed for almost every route it flew and

sometimes on routes it shouldn't fly. Its 400 seat range on four engines, sometimes didn't fill up the cabin for the fuel that was loaded, and then airlines wanted something better by going with less than 400 seats on just two engines. Then came the wide bodies. The 777 and

787 were more fitted for having less than capacity of tickets on routes that sometimes would become awkward to the financial bottom line. By having twin engine mid-bodies, the empty seat risk on having a four engine 747 was averted. First the

777 XWB and then the 787 came to the rescue, and now United Airlines will retire its

747's in 2017.

The two engine vs four engine and the 250 vs 450 seat

strategy is settled. Some like it cold and some like it hot. There is a time

and place for the right size and a seat number on every route, and every situation while not cramming 550 in an Airbus A-380 with so many is not the answer, and was a

bad business decision because the 747 already answered how many seats is

needed.

Boeing as an irritation and a stumbling block for the A-380, introduced the 747-8 on the cheap since it wasn't a clean sheet design and

didn't experiment with new technology, but used the already proven and

"paid for" 787 technology. The A-380 though, was a clean sheet design

trying to beat a 1960's Boeing Idea, the 747.

Boeing had long researched out how many seats for a given route is

best for a customer and came up with... well what they came up with was a twin

engine wide body. Then United Airlines just announced its retirement of the

venerable 747 during 2017. Perhaps this is the customers answer to Boeing's

decision of faking out Airbus and then it stumbles into Boeing's trick of playing off

the Euro's arrogance when it builds the world’s largest at something.

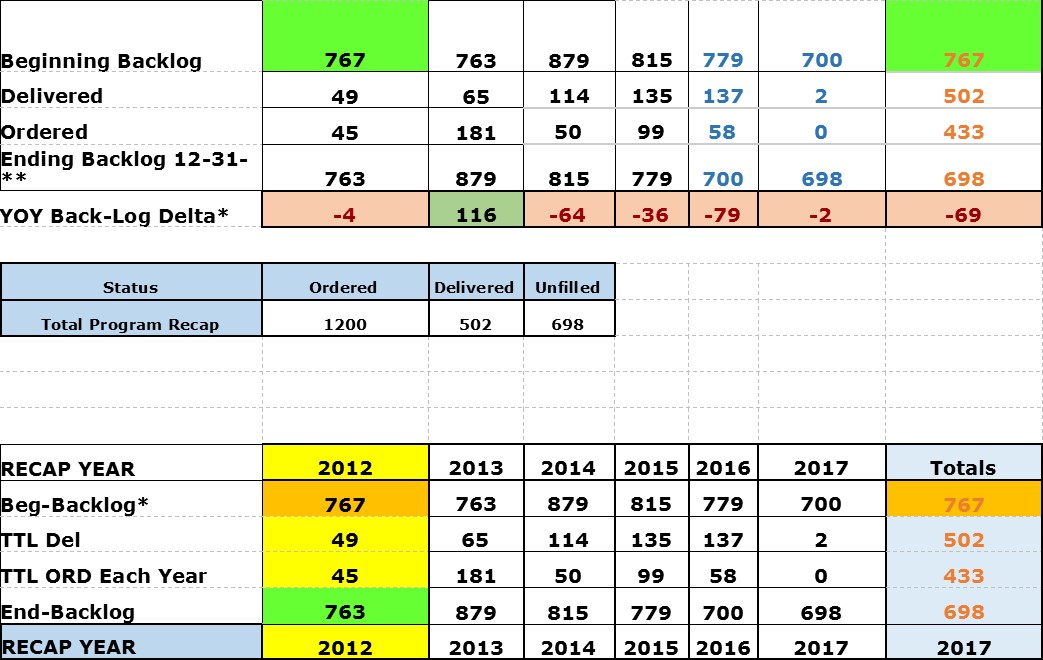

Billions invested in the behemoth and so few on backlog. In fact

there are more A-380 cancellations than orders over the last few years.

So many Airbus orders lost is an unintended consequence played out when introducing the 777X and the 787. Maybe Boeing research was right when planning only 250 seats

taking off twice a day giving passengers a choice of when to depart and having so many choices of where to fly. The common sense of it all beats getting-on only once a day during rush hour at unprepared terminals.

The seat spot was not consulted with when conceiving the A-380 own conventional wisdom. The 747 already had explored the seat potential and then

encouraged Airbus to keep up the good work when announcing once again, its

747-8i. At that moment, the A-380 was doomed as Boeing mopped up all its

leftovers the Airbus clan had hoped to capture. It lost the freight concept to the 747-8F.

It lost out to Boeing customers who would rather not have a double Airbus on the

side. It just lost out when pushing forward with some sort of mental momentum,

and now this, United retires its 747's!!!. The B team, "loves it when a

plan comes together". The newly renamed A-380 relishes in its moniker,

"The White Elephant". The soon to be renamed concept,

"night-mare liner" reaches the Airbus bottom line as it can't

complete its current backlog.

Most books count 319 A-380's ordered and it has delivered 200 of

its type. The backlog stands at 119 by most books tracking this disaster in the

"making". The 747 smiles on, "Been there, seen it, and done

that". It’s so 1970's, Airbus you rascal. Perhaps Airbus is a quick study

since they came out with Rolex (Rolodex) knock-offs called the A-350 800, 900, 1000,1100,

2000, "getting the picture of what it looks like to grasp at straws". An American

Indian customer named, "Tonto", would not trade for plastic cutlery

like the A-350, kemosabe.

Wikipedia:

"Ke-mo

sah-bee (/ˌkiːmoʊˈsɑːbiː/; often spelled kemo sabe or kemosabe)

is the term of endearment and inventive catchphrase used by the fictional

American Indian sidekick Tonto, in the American television program The Lone

Ranger. ... In the 2013 film The Lone Ranger, Tonto states that it means

"wrong brother" in Comanche."

Airbus has underestimated Boeing at every turn with its own air of

incompetence. Meanwhile back at the Boeing ranch, United Airlines will receive

more 787-9's this year and the 747 makes room on the flight line by retiring.

Having your seats in a row before you build something, is more important than

just being big.